It is often difficult to estimate how much money will be available at the end of a working life, as decisive factors change over the years.

Three decisive reasons for private pension provision:

Life expectancy is rising steadily, which is one of the important factors when it comes to old-age provision. As age increases, so does the need for capital. So if you don't want to retire later, you need to save enough capital to maintain a certain standard of living.

In addition to rising life expectancy, inflation also plays an important role in retirement planning. It causes savings to shrink and, according to the Federal Reserve Bank, will probably remain at around 2% in the coming years. If inflation remains constant, this would mean a devaluation of purchasing power from 1,000 euros to only around 550 euros within the next 30 years.

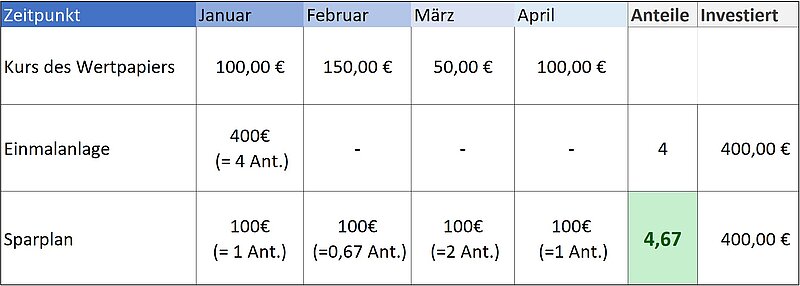

The cost-average effect is an effect created by regular investment of money (in the form of a savings plan). When prices fall, the investor buys more shares; when prices rise, he buys fewer shares. The individual partial purchases result in an average price, which in the best case is even lower than with a one-time investment. In any case, this form of investment avoids waiting for "perfect timing".

If you start early with private provision in addition to company and statutory provision, your assets can grow exponentially. The effect that comes into play with a long-term investment is the so-called compound interest effect. Profits that have already been earned generate renewed returns, causing the assets to grow exponentially - not linearly.